Bank statement processing is often treated as a simple data extraction task, but the real value starts after the transactions have been cleaned, categorized, and summarized.

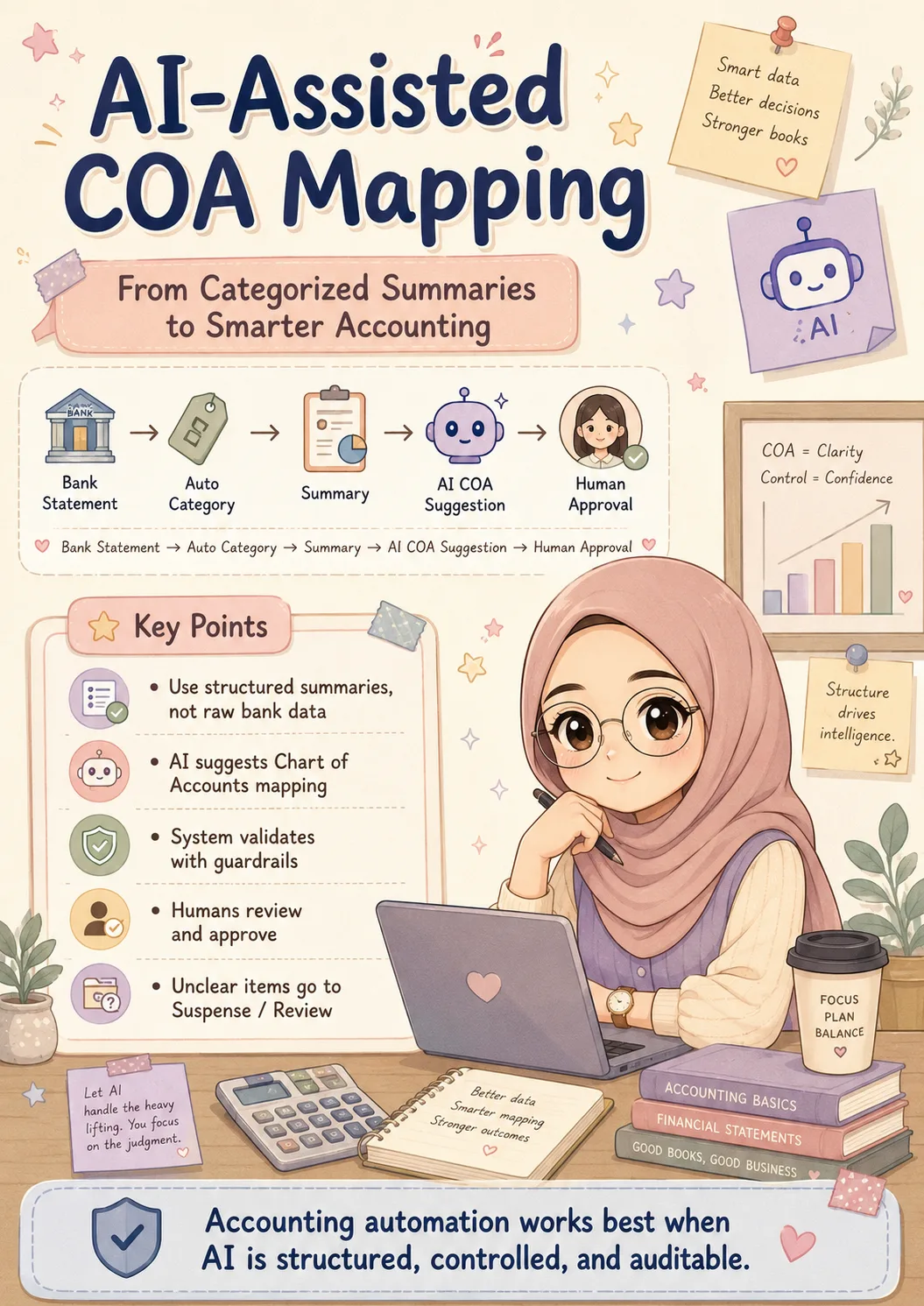

One useful next step is using AI to suggest a Chart of Accounts from categorized transaction summaries. Instead of asking AI to read raw bank statements directly, the system first processes the transactions, groups them by category, keyword, merchant, and transaction behavior, then sends only structured summaries to AI.

This approach is more practical because raw bank data usually contains too much noise. Descriptions can be inconsistent, merchant names can vary, and transaction purposes are not always obvious. When AI works from structured summaries, the output becomes more focused, more controlled, and easier to review.

For example, advertising-related transactions can be mapped to Advertising & Marketing Expense. Courier and delivery payments can be mapped to Delivery or Fulfillment Expense. Bank fees can be mapped to Bank Charges. Unclear transactions should not be forced into a random account. They should be placed under Suspense or Review for manual checking.

The key principle is simple: AI suggests, the system validates, and humans approve.

AI should not be allowed to freely create accounting accounts without control. Without guardrails, the Chart of Accounts can quickly become messy, duplicated, and inconsistent. A good system should first check whether a similar account already exists, apply confidence scoring, and route uncertain transactions for manual review.

This creates a cleaner accounting workflow: from bank statement, to transaction category, to summary, to COA mapping, and eventually to draft journal entries.

For SMEs, this kind of workflow can be very useful. Many small businesses still rely heavily on bank statements as their main financial record. Turning that data into a structured accounting format can reduce manual work, improve consistency, and make financial reporting easier to manage.

The goal is not to let AI “do accounting” blindly. The better approach is to place AI at the right point in the workflow, supported by validation rules, guardrails, and approval steps.

That is how accounting automation becomes realistic not magic, but structured, controlled, and auditable.